In a survey released in early 2018, only 37% of Americans said they would be able to pay for an unexpected $500-$1000 cost. 63% of respondents said they would need to resort to measures such as cutting back other spending, using a credit card, or borrowing money from friends or family in the event of a costly emergency. We have been writing for years on our position that people should not have to decide between health care or groceries or skipping prescriptions. There are ways to build a health spending plan to ensure you are financially able to pay for […]

Tag: Generic Drugs

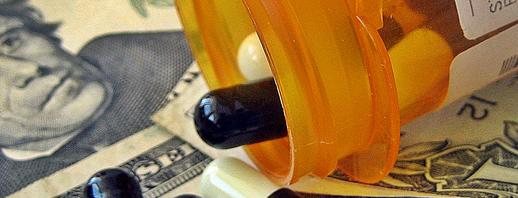

What is a Clawback & How it’s Affecting Your Prescription Copays

Americans may be surprised to learn that they could be paying more for their medications with their insurance copay instead of the cash price available to those without insurance. A study published last week found that Pharmacy Benefit Managers (PBMs) undermine claims that negotiated “rebates” with pharmaceutical companies are passed on to consumers. This follows a federal lawsuit filed over the summer after a California woman paid a $164 copay on a medication that can be purchased for $92 from the same pharmacy by anyone not using insurance. This practice is known as “clawback” and is instituted by PBMs who […]

How to Find the Best Prices for Prescriptions

We are almost to 2016, and the high costs of prescriptions are still a huge problem for millions of Americans. Despite laws like the Affordable Care Act (ACA), drug prices continue to vary and rise in ways that are often too much for patients to navigate. A recent poll found that a third of those currently taking a medication experienced a spike in price in the past year. Consumer Reports was able to uncover a lot of information with a national price scan of five common generic drugs. With their findings in mind, there are tips one can follow to […]

Introducing $4 Generic Discount Drug Programs

Earlier this year, we announced a project we would be releasing in 2015. After months of work and research, we are now offering information on discount generic medications. These $4 Generic Discount Drug Programs offer 30- or 90-day supplies of prescribed generic medications for prices as low as $4-$15. With over 120 of these programs nationwide, this is the first time information for them is searchable and available in one place. Using the new resource, one can search for prices for thousands of generic medications as well as programs in their area or national pharmacies such as Walmart, CVS, […]